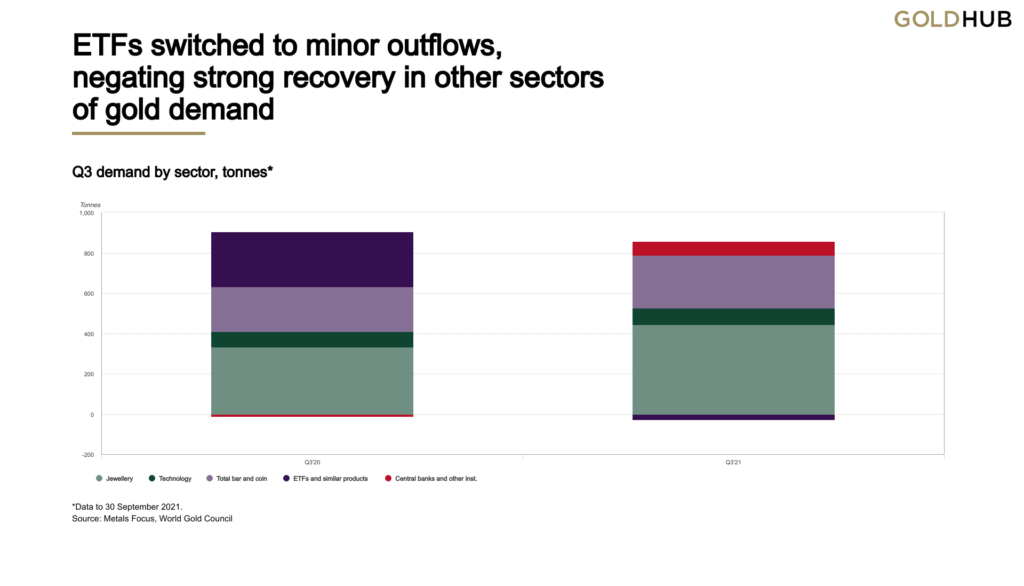

In the third quarter (Q3), global gold demand (excluding over-the-counter transactions) declined by 7% year-on-year (y-o-y) to 831 tonnes (t). This decline was primarily driven by exchange-traded funds (ETFs), which shifted from substantial inflows in Q3 2020 to modest outflows in 2021. Despite strong performance in other gold demand sectors—such as jewellery, technology, and physical investment in bars and coins—ETF movements significantly impacted overall demand.

Meanwhile, central bank purchases showed a solid improvement compared to Q3 2020, when there was a small net sale. On the supply side, total gold supply decreased by 3% y-o-y, largely due to a sharp decline in recycling activity.

Sector-Wise Gold Demand Breakdown

- Jewellery: Demand surged 33% y-o-y to 443t, supported by the ongoing global economic recovery. Consumers returned to purchasing gold jewellery as markets rebounded from pandemic-related disruptions.

- Bar and Coin Investment: Investment in physical gold increased 18% y-o-y to 262t, with many investors taking advantage of the sharp drop in gold prices in August as a buying opportunity.

- Gold ETFs: Small outflows of 27t had a disproportionately large impact on total gold demand, especially when compared to the significant 274t inflows recorded in Q3 2020.

- Central Bank Purchases: Global central banks continued accumulating gold, albeit at a slower pace. Total reserves increased by 69t in Q3, bringing year-to-date (y-t-d) net purchases close to 400t.

- Technology Sector: Demand for gold in technology grew 9% y-o-y to 84t, driven mainly by the ongoing recovery in the electronics industry. This figure is now aligned with pre-pandemic quarterly averages.

Macroeconomic Factors and Market Highlights

The average gold price in Q3 stood at US$1,789.5 per ounce, slightly lower than Q2 levels. Compared to the record-high gold prices of August 2020, this reflects a 6% y-o-y decline. The gold market’s performance mirrors its supply-demand dynamics and is influenced by broader macroeconomic factors, including rising interest rates and increased investor appetite for riskier assets.

Year-to-Date Trends and 2021 Outlook

- Total gold demand for the first nine months of 2021 is 9% lower y-o-y. A doubling of central bank gold purchases and 50% growth in jewellery demand helped cushion the decline, but they were not enough to offset the significant drop in ETF inflows.

- Gold supply has remained flat y-t-d. While mine production increased by 5%, a sharp 12% contraction in gold recycling has offset these gains.

- Full-year outlook: The ongoing economic recovery is expected to continue supporting jewellery and technology demand. Investment demand may benefit from inflation concerns, but ETF flows are likely to remain well below 2020’s record levels. Central bank purchases are on track to exceed the annual average, reinforcing gold’s role as a strategic reserve asset.

Conclusion

While gold demand across key sectors has strengthened, ETF outflows have dampened overall growth. With central banks increasing their gold reserves and jewellery demand rebounding, the market remains dynamic. However, the contrast with 2020’s exceptional investment-driven demand highlights the shifting landscape of gold consumption in the post-pandemic world.

Leave a Reply